Estimated reading time: 7 minutes

Would you rather listen to a podcast than read the article?

Table of contents

- Would you rather listen to a podcast than read the article?

- The Hiring-First Trap: Why More Bodies Make Accounting Firm Burnout Worse

- Root Cause #1: The Wrong Client Mix Is Burning Accounting Your Staff Out

- Root Cause #2: Manual Workflows Are Driving Accounting Staff Retention Off a Cliff

- The Two-Part Fix: How to Retain Accountants Without Hiring Your Way Out

- You Don’t Need to Outhire the Crisis. You Need to Outgrow It.

It’s Tuesday morning. You’re holding a fresh cup of coffee and a fresh resignation email from your second-best senior accountant. She’s leaving for a firm down the street that’s offering ten thousand more and a four-day work week. Accounting firm burnout is real.

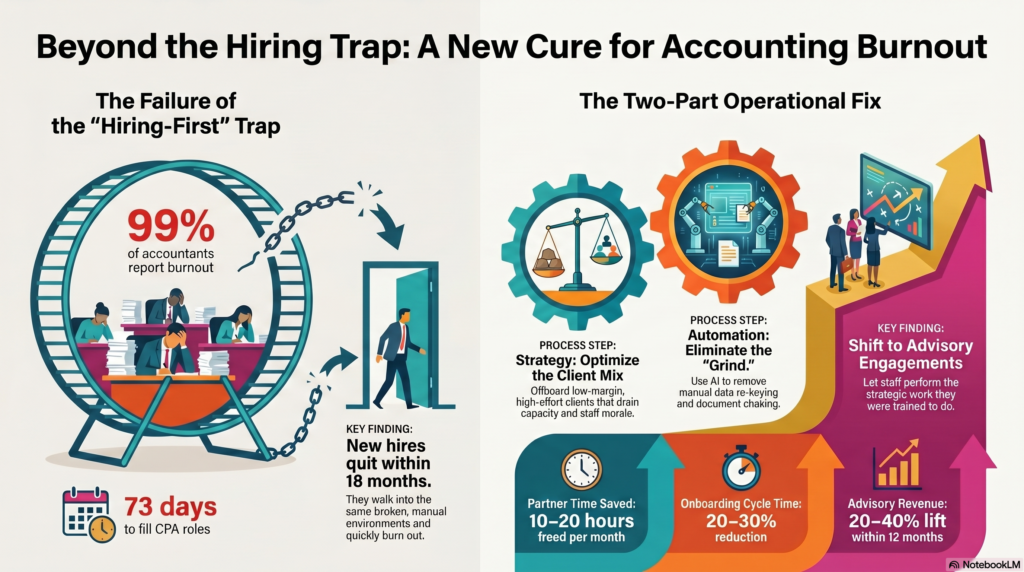

You’ve been here before. You’ll raise the offer for her replacement. You’ll call the recruiter. You’ll spend the next 73 days trying to fill the seat. And you already know — somewhere in the back of your mind — that the new hire is going to burn out in eighteen months and you’ll do this all again. Welcome the the accounting firm burnout hamster wheel.

We know how frustrating it is. You’ve raised salaries. You’ve added wellness stipends. You’ve done the happy hours. And your team is still running on fumes.

Here’s the contrarian truth almost no one in the industry is willing to say: this is not a hiring problem. Accounting firm burnout is a client mix problem and a workflow problem. And no amount of new hires will fix it.

This article walks through what’s actually causing burnout in 2026, why hiring more people often makes it worse, and the two-part fix that doesn’t require finding a single new accountant.

The Hiring-First Trap: Why More Bodies Make Accounting Firm Burnout Worse

The numbers tell a brutal story. CPA candidates are down more than 30% since 2016. Time-to-fill for CPA-required roles now averages 73 days — about 41% longer than comparable non-CPA positions. A FloQast study found that 99% of accountants report burnout, with nearly a quarter at moderate-to-severe levels.

When a partner sees those numbers and watches a top performer walk out the door, the reflex is predictable. Post the job. Raise the offer. Sign a recruiter. Throw money at retention bonuses for the staff who are left.

It rarely works. And here’s why.

The new hire walks into the same broken environment. The same overflowing client list. The same manual onboarding process. The same Excel spreadsheets being re-keyed into three systems. The same partners who are too busy to mentor anyone because they’re stuck doing tactical execution that should have been systematized five years ago.

So the new hire burns out in eighteen months. And the partner is back where they started, except now the firm has spent another six figures on recruiting, training, and severance.

You don’t have a talent supply problem. You have a workload composition problem. And until you fix the composition, every dollar you spend on hiring is rented growth, not owned growth.

Root Cause #1: The Wrong Client Mix Is Burning Accounting Your Staff Out

Most firms we work with are 60–70% loaded with low-margin, high-effort compliance clients. The kind that demand a lot, pay too little, and treat your team like a service vendor instead of a strategic partner.

This is what actually burns staff out. It is not “too much work.” It is too much of the wrong work.

Try this diagnostic. Pull your top ten clients by revenue and your bottom twenty by margin. The bottom twenty are the ones eating capacity. They are the ones forcing your senior accountant to work until 9 p.m. so a marginal client gets their quarterly the day they want it. They are the ones generating the urgent emails on a Saturday. They are the ones your team groans about at the standup.

And here is the hard truth. As long as those clients are on your books, you cannot pay your top performers what they are worth. The margin is not there. So your best people leave for the firm down the street that figured out how to fire its bottom twenty and reinvest in its top ten.

Right-fit clients pay more, demand less rework, and let your staff do the kind of advisory work they actually went to school for. Poor-fit clients do the opposite. The talent crisis is not an industry-wide problem you cannot solve. It is a client list problem you have not yet solved.

Root Cause #2: Manual Workflows Are Driving Accounting Staff Retention Off a Cliff

The second cause is even more solvable. 2026 is the year AI and automation move from experimentation to execution in finance and accounting. The Karbon State of AI in Accounting report found that confidence in AI for core processes is rising sharply this year, and Accounting Today calls it the year automation goes mainstream.

The firms keeping their best people are not the ones with the highest base pay. They are the ones using automation to eliminate the grinding manual work that drives turnover.

Think about where your senior accountant actually spends her week. How much of it is chasing PBC lists from clients who don’t respond? How much is re-keying data between QuickBooks, your practice management tool, and a spreadsheet someone built in 2019? How much is sending status update emails she could have automated? How much is scheduling meetings that a calendar tool could book on its own?

A staff member who spends 60% of her week on that kind of low-value, low-engagement work will leave. The firm next door that automated her onboarding intake, her reconciliations, and her client communication won’t lose her. It is not because they have a better culture. It is because their staff get to do real accounting.

Manual workflows are not a back-office inconvenience. They are an accounting staff retention problem disguised as an operations problem.

The Two-Part Fix: How to Retain Accountants Without Hiring Your Way Out

Here is what we have learned from working with managing partners across the country. The fix is not a recruiter. It is Strategy plus Automation, executed for you, so you don’t have to add another initiative to your already-impossible list.

Strategy. We define your right-fit clients with hard data — revenue, margin, hours, cross-sell potential, referral quality. We build the messaging that attracts more of them and the offboarding plan to gracefully shift the mix away from the poor-fit ones that are draining your team. Within twelve months, your staff are working on more advisory engagements and fewer firefights, and your margin per hour goes up.

Automation. We build the workflow systems that eliminate the grind. Client onboarding, document collection, reconciliation routines, status communication, internal handoffs. We integrate the tools you already have, plug in AI where it actually moves the needle, and free 10–20 partner hours per month while protecting staff capacity.

The RightFit difference is that we don’t hand you a deck and disappear. We do the heavy lifting. Partners stay involved in decisions, not execution — typically 2–4 hours of partner time per month. You don’t need another consultant telling you what to do. You need a partner who will actually do the work.

The results clients typically see: a 20–30% reduction in onboarding cycle time, 10–20 partner hours freed per month, and a 20–40% lift in advisory revenue within twelve months. That is how you keep your best people. Not with a signing bonus. With a firm that is actually worth working at.

You Don’t Need to Outhire the Crisis. You Need to Outgrow It.

Three takeaways.

First, the talent crisis is real, but hiring is not the answer. Every firm that tries to outhire it is paying for the same broken environment twice.

Second, your client mix and your workflows are what is actually burning your team out. Fix those, and retention takes care of itself.

Third, fixing both — without piling more onto already-overburdened partners — is exactly what RightFit was built to do. Strategy and Automation, executed for you, with measurable results in months, not years.

You don’t need another strategy. You need someone to make it work.

Schedule your Discovery Call. In 30 minutes, we’ll show you which clients are actually costing you your best people and which workflows are quietly draining your firm’s capacity. No deck. No homework. Just a clear picture of where your firm is leaking time and talent — and what to do about it.

Schedule Your Discovery Call →

Sources

- Wolters Kluwer — Accounting Firm Challenges 2026

- Accounting Today — Building the Firm of the Future: Key Shifts to Watch in 2026

- Robert Half — The Accountant Shortage Will Persist in 2026

- Talentfoot — How the CPA Shortage Is Extending Time-to-Fill

- Karbon — State of AI in Accounting 2026

- CPA Practice Advisor — Why Accounting Burnout Spikes in Summertime (2026)

- Vintti — 99% of Accountants Suffer From Burnout